Introduction: Life Insurance Is a Financial Tool—Until It Works Against You

Life insurance is often positioned as one of the most responsible financial decisions a leader can make. CEOs, executives, entrepreneurs, and high-income professionals are frequently advised to purchase life insurance early, commit long-term, and trust the system to protect their families, businesses, and legacy.

In theory, life insurance should provide certainty, risk transfer, and financial stability. In reality, many life insurance products are designed to optimize profits for insurers, not outcomes for policyholders. The problem is not always outright fraud—it is structural complexity, misaligned incentives, and information asymmetry.

Life insurance companies operate sophisticated business models. They understand that most policyholders:

- Do not read full contracts

- Do not reassess policies regularly

- Do not fully understand cash value mechanics

- Rarely challenge illustrations or projections

This article explores three common ways life insurance companies effectively “scam” policyholders—especially high earners—through legal, but strategically misleading practices. More importantly, it provides a CEO-level framework for protecting capital, making smarter insurance decisions, and avoiding long-term financial traps.

Way #1: Selling Complex Policies That Benefit the Insurer More Than You

1.1 The Problem With Complexity in Life Insurance

One of the most common tactics in life insurance sales is intentional complexity. Products such as whole life, universal life, and variable life insurance are often marketed as:

- “Investment + protection”

- “Tax-efficient wealth-building tools”

- “Lifetime coverage with cash value”

While these policies can be useful in very specific situations, they are frequently sold to individuals who do not need them, at a cost that significantly reduces long-term financial efficiency.

Complexity benefits the insurer because:

- Costs are hidden

- Performance is hard to evaluate

- Comparisons are difficult

1.2 Cash Value Illusions and Overpromised Returns

Many permanent life insurance policies include a cash value component, often marketed as:

- “Guaranteed growth”

- “Safe investment alternative”

- “Tax-free retirement income”

What is often not emphasized:

- Early-year returns are extremely low

- Fees are front-loaded

- Cash value growth is slow for 10–15 years

- Internal rate of return is often inferior to alternatives

In many cases, executives discover that after years of premiums, their cash value is far below expectations.

1.3 Who Actually Benefits From These Policies?

These products often benefit:

- Insurance companies (long-term premium streams)

- Agents (high commissions in early years)

They are rarely optimized for:

- Liquidity

- Flexibility

- Capital efficiency

For CEOs and entrepreneurs, capital tied up inefficiently represents opportunity cost, not protection.

1.4 CEO-Level Protection Strategy

Smart leaders:

- Separate insurance from investing

- Use life insurance strictly for risk transfer

- Avoid unnecessary complexity

In most cases, term life insurance + disciplined investing delivers superior outcomes.

Way #2: Overcharging You Through Commissions, Fees, and Policy Design

2.1 The Commission Structure You’re Not Shown

Life insurance is one of the most commission-heavy financial products in existence.

Typical commission realities:

- Agents may earn 50%–100% of your first-year premium

- Ongoing trailing commissions are common

- Incentives favor selling larger, more complex policies

These commissions are rarely transparent—and are embedded into your premiums.

2.2 Front-Loaded Costs That Destroy Early Value

Many policies are designed so that:

- Early premiums primarily pay commissions and fees

- Cash value accumulation is delayed

- Policy surrender in early years results in losses

From a CEO perspective, this structure violates basic capital efficiency principles.

2.3 Policy Illustrations: Legal, But Misleading

Insurance illustrations often assume:

- Optimistic interest rates

- Ideal market conditions

- No changes in cost structures

While legally compliant, these illustrations can create false confidence. Actual performance frequently underdelivers.

2.4 The Long-Term Cost of “Set and Forget” Insurance

Most policyholders never review their policies after purchase. Over time:

- Fees accumulate

- Coverage becomes misaligned with needs

- Better alternatives emerge

Insurance inertia is profitable—for insurers.

2.5 CEO-Level Protection Strategy

Executives protect themselves by:

- Demanding full cost transparency

- Requesting internal rate of return (IRR) projections

- Reviewing policies every 3–5 years

- Using fee-only advisors for second opinions

Leadership requires oversight—even in personal finance.

Way #3: Locking You Into Long-Term Commitments That Reduce Flexibility

3.1 The Illiquidity Trap

Many life insurance policies are illiquid by design. Exiting early often means:

- Surrender charges

- Loss of principal

- Tax consequences

This structure discourages policyholders from leaving—even when the policy no longer serves their interests.

3.2 Changing Life, Static Policies

Executives’ lives evolve rapidly:

- Business growth or exit

- International relocation

- New dependents

- Wealth accumulation

Yet many policies are rigid, making it costly to adapt coverage to new realities.

3.3 Borrowing Against Your Own Policy

Some insurers promote policy loans as a benefit. However:

- Loans accrue interest

- Poor management can collapse the policy

- Death benefits may be reduced

This is not “free money”—it is leverage against your own capital.

3.4 Opportunity Cost at Scale

For high-income individuals, the opportunity cost of locking capital into underperforming policies can reach:

- Hundreds of thousands

- Or even millions over decades

Capital trapped is capital that cannot compound elsewhere.

3.5 CEO-Level Protection Strategy

Sophisticated leaders:

- Prioritize flexibility

- Avoid long-term premium commitments without exit options

- Align insurance duration with actual risk exposure

Insurance should adapt to leadership—not constrain it.

Why These Practices Continue

Life insurance companies succeed because:

- Information asymmetry favors insurers

- Complexity discourages scrutiny

- Emotional selling overrides rational analysis

Most policies are sold—not strategically chosen.

How CEOs and Executives Should Approach Life Insurance

Strategic Principles

- Insurance is not an investment

- Risk transfer is the primary function

- Liquidity and flexibility matter

- Simplicity scales better

Best Practices for Smarter Life Insurance Decisions

1. Start With the Risk

Ask:

- Who depends on my income?

- For how long?

- How much capital is required?

2. Match Duration to Need

Most life insurance needs are temporary—not lifelong.

3. Demand Transparency

Understand:

- All fees

- Commissions

- Break-even timelines

4. Review Regularly

Your insurance should evolve with your leadership journey.

SEO Keywords (Suggested)

Primary keywords:

- Life insurance scam

- Life insurance company tricks

- Life insurance hidden fees

- Life insurance for CEOs

Secondary keywords:

- Whole life insurance problems

- Life insurance commissions

- Term vs whole life insurance

- Life insurance mistakes executives make

Conclusion: Life Insurance Should Protect Your Legacy—Not Drain It

Life insurance is a powerful financial tool when used correctly. But when sold through complexity, excessive fees, and inflexible structures, it can quietly erode wealth instead of preserving it.

For CEOs, executives, and entrepreneurs, the solution is not to avoid life insurance—but to approach it with the same discipline applied to business decisions.

Clarity beats complexity.

Flexibility beats long-term lock-in.

Strategy beats salesmanship.

The most dangerous insurance policy is the one you never question.

Word Count:

348

Summary:

Although it makes sense to get in touch with a life insurance company to cover your dependents in the eventuality of your untimely death, there are integrity issues surrounding the insurance companies and agents.

Keywords:

online life insurance quote, life insurance

Article Body:

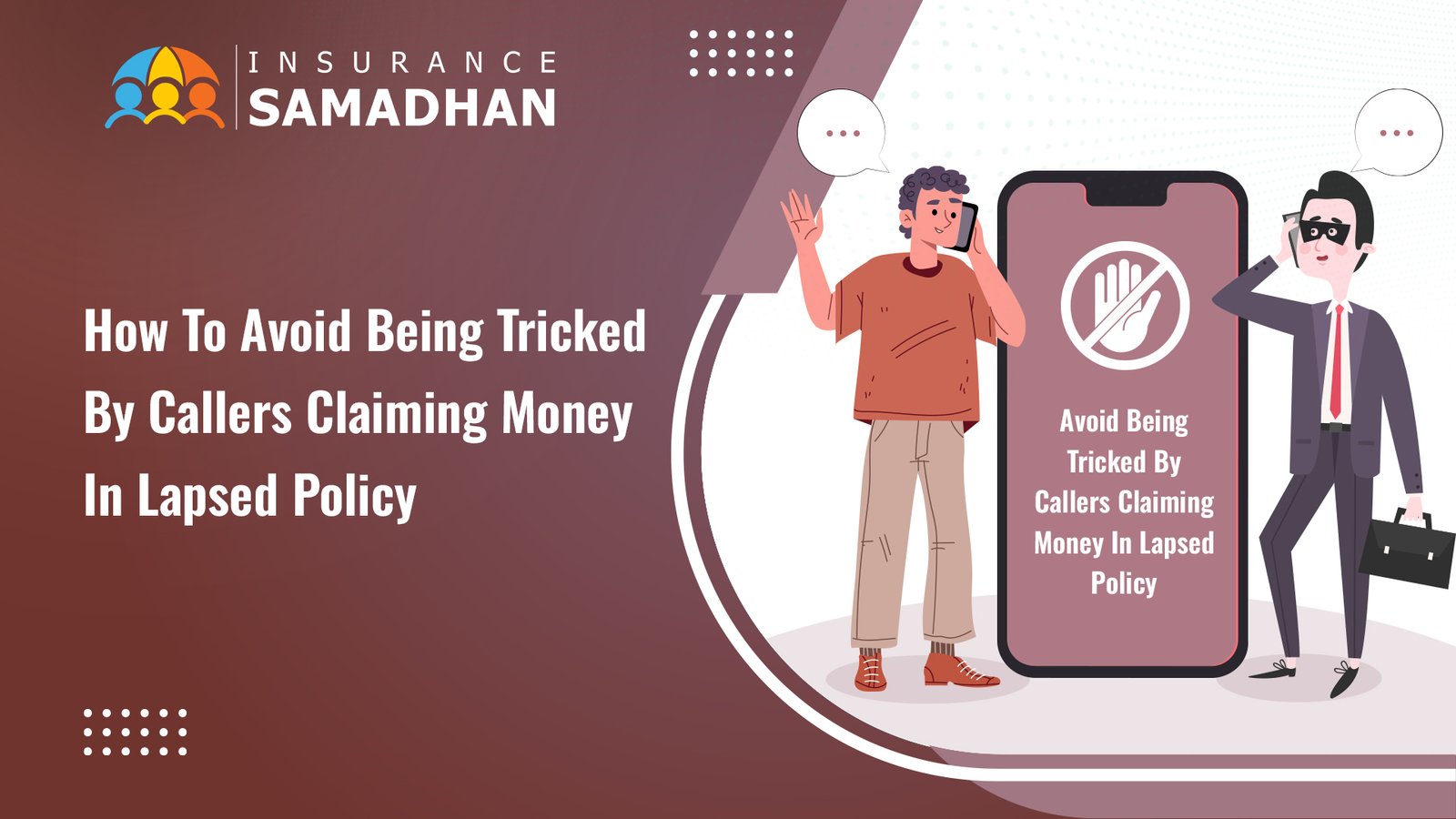

Although it makes sense to get in touch with a life insurance company to cover your dependents in the eventuality of your untimely death, there are integrity issues surrounding the insurance companies and agents. Broadly there can be 3 ways your life insurance company is scamming you. We have enlisted them for your benefit.

Selling Coverage that you don�t need!

The insurance companies thrive on the fact that most people don�t understand their life insurance needs. With standard products, they try to sell you coverage that you might not need, but, which are lucrative for them. The insurance agents expedite the process so that you skip the fine print and sign up for a coverage that is ill-suited to your needs. The trick is to play on your fear factor and sell you heavy insurance, even if you don�t have dependents.

Coaxing you to pay �Cash�

We strongly suggest, do not pay your premium through cash to an agent. Further, do ensure that you get a receipt for the payment. There are numerous fraudulent entities posing as genuine insurance agencies that extract hard cash from you in lieu of insurance premium. They ask you to sign at blank spaces in a form, assuring you that it is just a formality. Once you have fallen for their trick, you are left without an insurance coverage. The worst part is that most victims only come to know of this scam, when they have met with some mishap and there is not insurance to cover them.

Luring you with benefits!

Insurance agencies and agents have a way of promising you unbelievable benefits out a life insurance policy. Life insurance agents might offer you plans, with a guarantee that the policy would run premium-free for a specific period. Some agents play it smart and offer you great discounts for signing you up for a new policy, while replacing an old policy. The trick is that the old coverage gets terminated and new coverage does not get initiated due to the cumbersome procedural bottlenecks. Thus, exposing you to risk without cover.

Tinggalkan Balasan